1 Growth Stock Down 50% to Buy Right Now

Some investors took one look at The Trade Desk‘s (NASDAQ: TTD) fourth-quarter results and slammed the sell button. The digital advertising expert missed Wall Street’s consensus revenue target for the first time since the company went public in 2016. The stock closed 33% lower the next day, erasing a year’s worth of market-beating gains. Right now, The Trade Desk’s stock is down 50% from its annual peak.

Bargain alert: The Trade Desk is on sale!

In my eyes, that’s a wide-open invitation to buy this top-quality growth stock. It’s still not a cheap stock, trading at 90 times trailing earnings and 14 times sales. But that’s way down from recent peaks, with price-to-earnings (P/E) ratios often soaring above 200 and price-to-sales (P/S) figures briefly peeking above 30. So, from a historical point of view, The Trade Desk’s shares look quite affordable right now.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

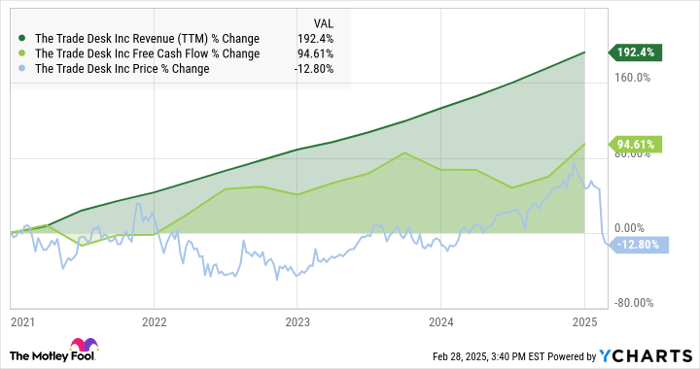

And you can’t forget about the company’s massive growth potential. Remember the inflation crisis that led to a bear market in 2022? The Trade Desk’s stock followed the market lower, but you wouldn’t have guessed that if you were looking at the company’s business results. The blue price chart in the graph below shows you the market action, but do you even see a slowdown in The Trade Desk’s sales growth? Meanwhile, its cash profits continued to trend upward:

TTD Revenue (TTM) data by YCharts. TTM = trailing 12 months.

A 15-step recovery plan

So, The Trade Desk’s annual free cash flows have approximately doubled in four years, while revenues have nearly tripled. The stock is 12% cheaper over the same span.

Yes, the company disappointed investors with slow sales growth and modest forward-looking guidance in the last earnings report. The brutal market reaction seems misplaced, though. The rare revenue miss was a 22.3% year-over-year revenue jump, falling just short of a 25.2% growth target.

Management did exactly the right thing. CFO Laura Schenkein took “full ownership” of the revenue miss on the Q4 earnings call. It wasn’t a missed opportunity but a period of relatively weak execution. In response, The Trade Desk laid out a detailed 15-point plan to kick the stalled sales growth into higher gear. The points of action include partnerships, audio ads, hirings in the sales department, and a tweaked process for product development.

The Trade Desk is not taking this slowness in stride. The company is taking resolute action to get back on track.

Paying a premium for an exceptional company

I can’t promise that The Trade Desk’s challenges will fade out in 2025, and some investors would say the stock remains too expensive even now. However, you’re paying a premium for a high-octane growth stock. This one earns an extra gold star for its positive earnings and cash flows — many businesses with the pedal to the metal tend to accumulate bottom-line losses until they’re ready to slow down and collect profits.

The Trade Desk is growing fast and making a profit at the same time. This combination alone deserves a significant price premium. Moreover, the company remains an innovator in the digital advertising technology space. Its Unified ID 2.0 (or UID2) standard is gaining support across the internet, helping advertisers and ad-spot sellers prepare for a radically changed ad market as Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) is forced to limit the utility of its ad-tracking services.

So, I don’t mind paying a pretty penny for The Trade Desk’s stock. In the future, I might remember the spring of 2025 as a time when this fantastic growth stock was available at a discount. This top-shelf growth stock should serve you well in the long run, especially if you start your position at today’s fairly modest price.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $323,920!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $45,851!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $528,808!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of February 28, 2025

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Anders Bylund has positions in Alphabet and The Trade Desk. The Motley Fool has positions in and recommends Alphabet and The Trade Desk. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.