Nvidia Stock Is Down 20%. Is It Time to Buy the Dip on the AI Leader?

It’s been a rough start to the year for Nvidia (NASDAQ: NVDA) shareholders. As of this writing, shares are down about 12% year to date and 20% below its January highs. The news from the company must be bad, right?

Well, not exactly. Late last month, Nvidia reported fourth-quarter and full-year earnings for its fiscal 2025 period, which ended Jan. 26. The news was good, not bad. Nvidia impressed analysts and investors once again by exceeding both top- and bottom-line estimates. Guidance called for another jump in revenue in the current quarter to a record $43 billion. So, let’s look at what has the stock plunging in 2025.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Market correction = opportunity

Some of the same things that have driven the Nasdaq Composite into correction territory have caused fear and uncertainty around Nvidia stock. The Trump administration has announced — and changed — several applications of import tariffs that could affect Nvidia’s business. On top of that, national security concerns have raised the prospects for more export restrictions on Nvidia’s powerful artificial intelligence (AI) chips.

The tariffs themselves could have both direct and indirect implications for Nvidia. There are concerns that tariffs could hinder economic growth and create an inflationary environment. Either of those situations could negatively impact semiconductor chip sales. After all, if a company building out data center capacity believes returns on investments will be impacted, it may very well reduce or delay those investments.

Nvidia’s share price skyrocketed over the last 18 months as investors forecast impressive revenue growth to continue. It’s been nothing short of amazing. Sales began to soar in 2023. Revenue jumped 126% in fiscal 2024, ending Jan. 28, 2024. It didn’t slow down in fiscal 2025, either. Growth of another 114% for that period ended this January, and the stock continued to run higher.

That is, until recently.

Nvidia investors shouldn’t worry

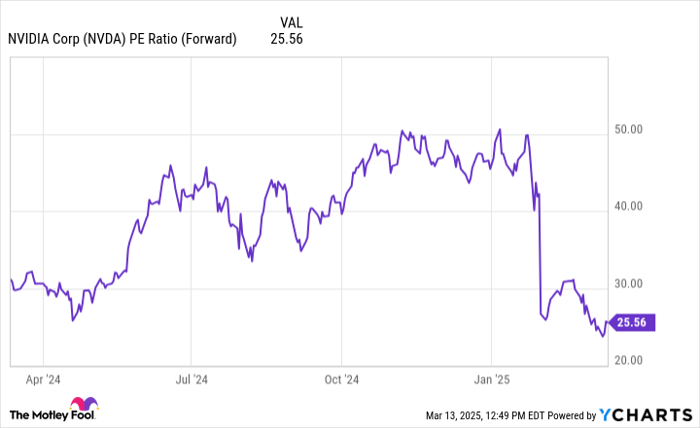

The 22% drop from its January high mark might just be a great opportunity for those who feared they missed out on owning Nvidia stock. As of this writing, it was trading at a price-to-earnings (P/E) ratio of just about 25 based on calendar year 2025 earnings. That’s pretty attractive compared to the 10-year average P/E of 32 for the Nasdaq-100 index.

That’s its lowest level since earnings estimates skyrocketed early last year. The stock itself has more than doubled since the start of 2024.

NVDA PE Ratio (Forward) data by YCharts

Nvidia still has plenty of opportunities for growth. Barring any major development of a trade war or recession, revenue should increase about 50% this year. That’s mostly driven by the Blackwell AI architecture, which is now in full production. There are many business development possibilities beyond that.

Nvidia touches most everything

The Rubin platform will succeed Blackwell with an even more powerful AI suite of offerings. But AI is more than just data center computing power, too. Companies developing autonomous vehicle (AV) technology are also loading up on Nvidia’s products for training purposes. The company says all 30 of the existing top AV data centers are powered by it.

Revenue in its gaming segment grew to over $11 billion last year. More than 200 million gamers and creators use Nvidia GeForce GPUs (graphics processing units). Millions of developers have downloaded its Monai open-source framework for healthcare imaging AI. Perhaps most potential will come from robotics as businesses utilize that evolving technology to improve efficiency. Nvidia says over 1.3 million developers already use the Nvidia Jetson high-performance computer platform for tasks including robotics, computer vision, and generative AI.

Nvidia has many irons in the fire. While revenue growth will slow to about 50% this year, its lineup of AI chips and software stacks is unmatched and constantly improving. Add in the possible catalysts from other segments, and its very reasonable recent valuation, and it looks like a compelling time to buy the dip in Nvidia stock.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $315,521!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $40,476!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $495,070!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of March 14, 2025

Howard Smith has positions in Nvidia. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.