Prediction: Ulta Beauty Stock Will Beat the Market. Here’s Why.

The market hasn’t been too happy with Ulta Beauty (NASDAQ: ULTA) stock recently. The beauty megachain’s shares are down 32% over the past year, seriously underperforming the S&P 500.

As if pressured conditions and performance weren’t enough, Berkshire Hathaway completely sold out of its position in the 2024 fourth quarter after slashing its stake in the second quarter, just one quarter after taking a position in the first place.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Altogether, it’s enough to scare away many an investor. But you can often find excellent opportunities where no one else is looking. And despite what’s happening right now, Ulta can still beat the market. Here’s why.

The leader in specialty beauty

Ulta operates a U.S.-based chain of 1,400 specialty beauty stores. If you didn’t know about the industry, you might not realize that Ulta’s model was original when it started, and it stands out for its differentiated approach to beauty still today.

In contrast to the typical beauty retail model, Ulta houses everything together under one roof. Most of the beauty industry is fragmented, with many separate categories sold individually. Luxury cosmetics are typically sold in outlets targeting the affluent consumer, and mass cosmetics are sold predominantly in pharmacies and at discount retailers, as an example. Ulta went against the classic retail model and brought everything together. The concept rests on the idea that there is a beauty enthisiast who buys from all the these categories, and that’s Ulta’s target customer. Adding to that approach, it also offers services, another innovation in beauty retail.

Ulta knows its customers, and its customers are loyal. Its so-called beauty enthusiasts have doubled in number to 140 million over the past three years, and they’re increasingly signing up for memberships. It has 44 million members as of the end of the most recent quarter, a 9% increase year over year, and they account for 95% of sales. Spend per member increased 11% year over year. These are the consumers that will bring it into its long-term potential.

Getting back to growth

This approach has worked well for Ulta until recently. Many retailers have felt tremendous pressure from inflation, Ulta included, and its operating margin has been squeezed. Not only did operating margin fall from 13.1% to 12.6% in the 2024 fiscal third quarter (ended Nov. 2), but operating income also fell from $327 million to $319 million.

It’s still reporting higher revenue and higher comparable sales (comps), which came in at 1.7% and 0.6% year over year, respectively, in the third quarter. Customers are still shopping at Ulta, but they’re likely to be shopping less and switching down to cheaper brands right now.

However, you can’t pin all of its woes on external factors. It’s also facing tough competition in its prestige market. Management said that there have been around 1,000 new retail points in the prestige range, and these are taking market share. In the most recent quarter, it seems to have found its footing, and management said that market share movement was flat in the third quarter. This is a development to track.

It’s taking several actions to improve its near-term position, such as expanding its product assortment and enhancing the user experience. It recently got a new CEO, and investors will hear about progress in the fourth-quarter report in early March.

A top find in the bargain bin

Ulta has a solid business and is still opening up new stores. It’s also attracting more members, and these are customers who are likely to spend, providing organic long-term growth opportunities. The beauty industry is expected to increase at a compound annual growth rate (CAGR) of 6% through 2028 according to McKinsey, and Ulta is well positioned to benefit from higher industry growth.

Will it bounce back quickly when inflation finally moderates? Will the new CEO be able to fix some of its problems? None of these are guarantees, but Ulta has demonstrated excellence over many years and has a long track record of strong performance under better circumstances.

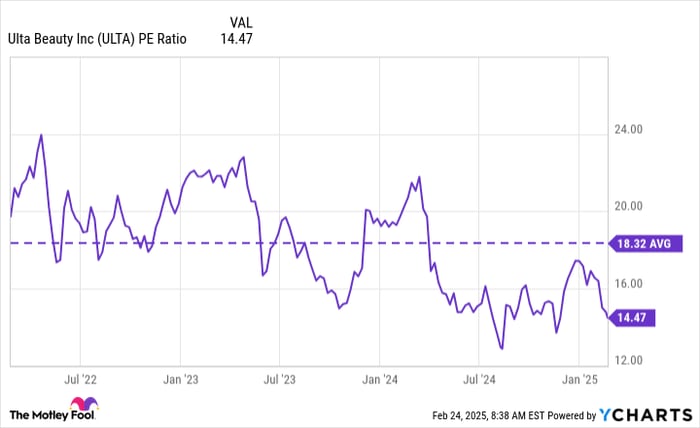

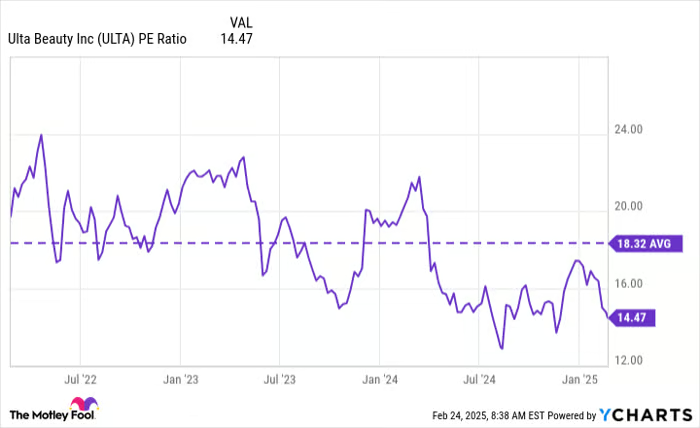

What makes the argument stronger is that Ulta stock is trading at a cheap price right now, and it’s not surprising that Buffett or one of his investing directors found it compelling. It very much fits into the Buffett schema of finding undervalued bargain stocks, trading at a P/E ratio of 14, well below its three-year average.

ULTA PE Ratio data by YCharts

Ulta has a long future ahead of it, and because the stock is down in the dumps, it has all the more opportunity to beat the market when it bounces back.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $311,551!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,990!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $519,375!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of February 28, 2025

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway and Ulta Beauty. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.