CrowdStrike Holdings (NASDAQ: CRWD) stock has witnessed a solid jump of 52% in the past six months, outpacing the Nasdaq-100 Technology Sector index’s gains of 6.5% handsomely during this period as the company’s recent results have been good enough to boost investors’ confidence following an IT outage in July last year that sent its shares plunging.

This impressive rally has brought CrowdStrike’s share price to just over $400. Does this mean this cybersecurity company could consider splitting its stock? Let’s find out.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Why CrowdStrike management may consider executing a stock split

A forward stock split is nothing but a cosmetic move that’s used to bring down the price of each share of a company by increasing the number of outstanding shares. For instance, if you hold one share of CrowdStrike and management announces a 2-for-1 stock split, you will have two shares once the split comes into effect. However, the value of your holdings won’t change as the price of each CrowdStrike share will be halved following the split.

So, a stock split does nothing to alter the market cap and fundamentals of a company, nor does it impact its prospects. However, there is a belief that a forward stock split makes the shares of a company accessible to a wider pool of investors by lowering the price. That could increase the demand for a company’s stock.

This is the reason why many companies have been undertaking stock splits in recent years. CrowdStrike hasn’t gone down that route yet since making its stock market debut in June 2019. However, management can consider a stock split for the reason pointed out in the previous paragraph, as a hypothetical increase in demand for CrowdStrike’s shares following a split may help it sustain its momentum.

But then, many brokerages allow investors to buy fractional shares, making the concept of a forward stock split redundant. That’s why we need to focus on important aspects such as CrowdStrike’s growth potential and its valuation to understand if it is worth buying the stock now, irrespective of a split.

Is this high-flying cybersecurity stock worth buying now?

The biggest red flag for anyone looking to buy CrowdStrike right now is its valuation. It is trading at a whopping 27 times sales and 94 times forward earnings. You may be wondering if CrowdStrike could justify these expensive multiples by delivering robust bottom-line growth.

However, that may not be the case, as the compensation packages that the company rolled out in the aftermath of last year’s outage are negatively impacting its business. CrowdStrike anticipates that its new annual recurring revenue (ARR) and subscription revenue were impacted to the tune of $30 million in the recently concluded fourth quarter of fiscal 2025.

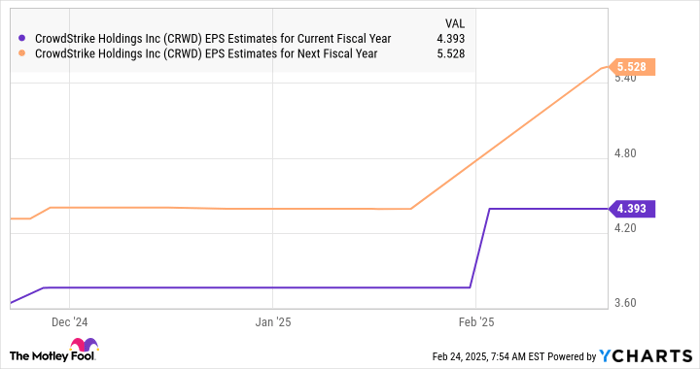

CrowdStrike also points out that it will be fulfilling more of its compensation packages in the coming quarters. This explains why analysts are forecasting a 17% increase in CrowdStrike’s earnings in the current fiscal year to $4.39 per share, following an estimated jump of 22% in fiscal 2025. However, an acceleration is expected in the next fiscal year.

CRWD EPS Estimates for Current Fiscal Year data by YCharts

The consensus estimate for fiscal 2027 suggests that the cybersecurity specialist could witness a 26% increase in earnings. While that’s healthy, it doesn’t seem enough to justify its expensive valuation. Assuming CrowdStrike does hit that mark in fiscal 2027 and trades at 34 times earnings at that time (in line with the tech-laden Nasdaq-100 index’s earnings multiple), its stock price would be $188.

That’s well below where CrowdStrike is trading right now. However, if there is a significant correction in CrowdStrike stock and it becomes available at a cheaper valuation, it may become worth buying for the long run thanks to the increasing adoption of its cybersecurity platform and the huge addressable market that it is targeting.

For instance, the number of customers using six or more modules of the company’s cloud-based Falcon cybersecurity platform increased by two percentage points year over year in the last reported quarter, along with an identical increase in those using seven or more modules. This led to a 27% year-over-year increase in the company’s annual recurring revenue in the quarter to just over $4 billion.

As ARR refers to the annualized value of CrowdStrike’s subscription contracts at the end of a quarter, the healthy year-over-year growth in this metric is a positive development. Management believes that it can hit $10 billion in ARR over the next six years, and it could very well achieve that mark, considering that it sees its total addressable market (TAM) hitting $250 billion after four years.

The company’s full-year revenue guidance of $3.93 billion for the recently concluded fiscal 2025 indicates that it could be scratching the surface of a huge opportunity. That’s why it won’t be surprising to see CrowdStrike sustaining a strong level of earnings growth in the long run.

However, it is difficult to justify this cybersecurity stock’s valuation right now as there are companies with faster growth rates available at more attractive valuations. As such, savvy investors would do well to keep CrowdStrike on their watchlists and consider buying it when it becomes cheaper or when there are signs of an acceleration in its growth.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $328,354!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,837!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $527,017!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of February 24, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.