This Recession-Resistant Stock Is Up 16% This Year. Here’s Why It Can Beat Trump’s Tariffs.

Spring is only just starting to bloom, but 2025 is already starting to look like a lost year for investors. As of April 8, the S&P 500 (SNPINDEX: ^GSPC) is down 18%, the Nasdaq Composite is in a bear market, and investors are reeling over President Donald Trump’s plan to impose the highest tariff rates in over a century.

Over the last week, all but five S&P 500 stocks are in the red, and of those, there’s only one that isn’t a healthcare company. It’s a retailer with a business model that makes it recession-resilient. In fact, it has a history of outperforming and seeing stronger growth in recessions, and it’s well positioned to avoid any headwinds related to tariffs.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

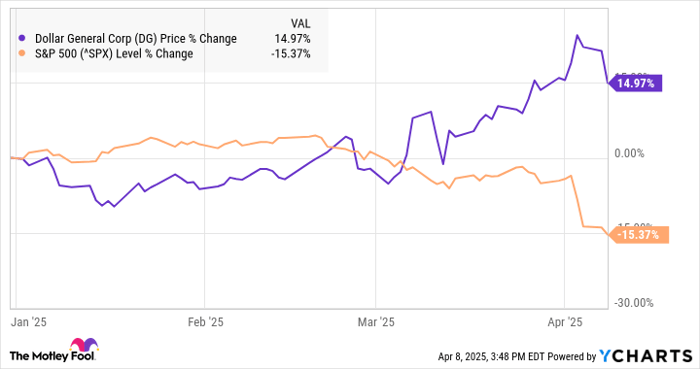

I’m talking about Dollar General (NYSE: DG), the discount retailer that suddenly looks like a winner after stumbling through 2023 and 2024. As you can see from the chart below, Dollar General has surged this year, easily beating the broad market:

Dollar General has gained as the S&P 500 has fallen, showing off its countercyclical nature. The stock surged the day after Trump announced global tariffs, gaining 4.7% even as the rest of the market tumbled, a sign that the market views Dollar General as tariff-proof.

Why Dollar General can beat tariffs

At the current moment of uncertainty in both trade policy and the overall health of the economy, Dollar General finds itself in an advantageous position, especially compared to other retailers.

First, consumables make up the vast majority of the company’s sales — 82% in 2024. These are products like paper and cleaning products, packaged food, perishables, and health and beauty products, all of which consumers buy in good times and in bad.

Because so much of its sales come from food, which is typically produced domestically, the company has much less tariff exposure than most retailers. According to Citigroup analysts, just around 10% of its inventory is exposed to tariffs, much better than Dollar Tree‘s 50%, as the latter company tends to sell more discretionary items.

Dollar General also has a history of outperforming in a recession, as consumers tend to trade down from more expensive stores when they’re looking to save money. Additionally, the retailer has the advantage of selling smaller package sizes, so consumers can buy single rolls of toilet paper or paper towels, which they couldn’t do at a competitor like Walmart.

In the throes of the great financial crisis, Dollar General reported same-store sales growth of 9% in 2008 and 9.5% in 2009, showing how consumers flock to its stores to save money. Over its history, the company has delivered positive same-store sales growth in every year since 1990, except for 2021 (a same-store sales spike of 16.3% when COVID-19 hit in 2020 gave way to a decline of 2.8% the following year). That track record shows it can do well in any economy.

Image source: Getty Images.

Is Dollar General a buy?

As a business, Dollar General has been struggling over the last two years. It’s lost market share to Walmart, and has seen margins fall sharply as inflation weighed on consumer spending in the low-income demographic.

The company announced a “Back to Basics” strategy, aiming to streamline its supply chain by closing temporary storage facilities and to improve store operations by reducing out-of-stock situations and making sure the point-of-sale area is adequately staffed. It’s also investing in more store remodels even as it continues to open new stores.

Dollar General finished 2024 with same-store sales growth of 1.4%, showing that demand is still improving, despite its margin challenges. Its 2025 guidance for same-store sales growth was a range of 1.2% to 2.2%. It also expects a modest rebound in earnings per share of $5.10 to $5.80 this year, compared to $5.11 in 2024.

The current economic environment could prove to be a tailwind for Dollar General, especially if concerns about a recession spread.

For investors, the stock remains well-priced at a price-to-earnings (P/E) ratio of 17. Additionally, it offers a current dividend yield of 2.6%.

With the uncertainty around the Trump tariffs likely to continue, Dollar General looks like a great stock to ride out the storm, and to beat the market if the economy continues to weaken.

Should you invest $1,000 in Dollar General right now?

Before you buy stock in Dollar General, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dollar General wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $495,226!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $679,900!*

Now, it’s worth noting Stock Advisor’s total average return is 796% — a market-crushing outperformance compared to 155% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of April 10, 2025

Citigroup is an advertising partner of Motley Fool Money. Jeremy Bowman has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Walmart. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.